- Suite 17 / 79 Manningham Road, Bulleen VIC 3105

- 0406 197 099

- hello@pmafinance.com.au

How to budget for a home on a low income

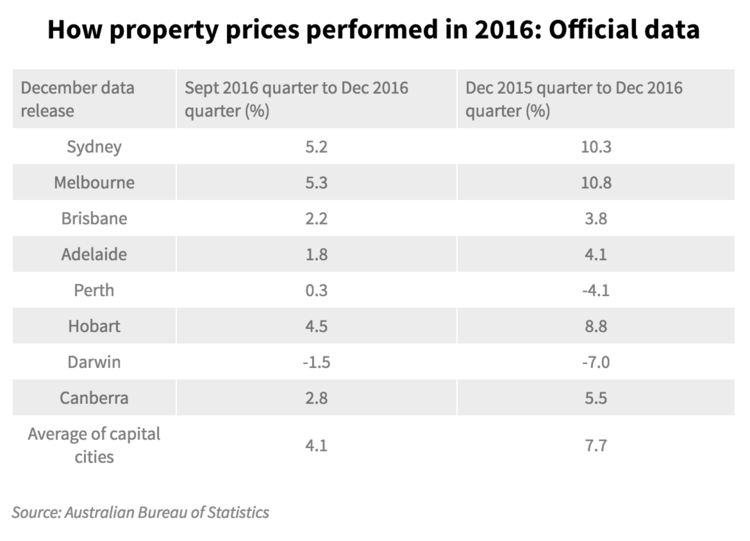

RBA ready to do more to cut economic risks off housing market

17/03/2017

Westpac joins NAB in raising interest rates

19/03/2017

If you’re slogging it out in a 9-to-5 job for what feels like a pittance, you’ve got the double whammy of rising house prices and a low income, and the goal of home ownership can seem even more hopeless.

According to the Australian Bureau of Statistics, the average annual earnings for Aussie employees is just over $60,000, a level at which the tax office gives you a low-income tax offset. So there are plenty of others out there scratching their heads, wondering how they are ever going to get into the market.

Others, however, are adjusting their notion of the Great Australian Dream so that it no longer looks like a big house in the ‘burbs with a Hills Hoist, but instead perhaps an apartment close to amenities. This is driven not only by affordability but by our changing lifestyle, too. So as hard as it might seem, don’t be disheartened.

I can allay your fears by telling you that yes, you can escape the rental market and buy your own home one day, but to make your dream a reality, you will have to change your mindset. Repeat after me: “I think I can. I think I can. I think I can. I know I can.”

While this might sound like a silly hippie chant, you’d be surprised at what a little positive thinking can do. Mostly it can spur you into action.

Start with a definite goal, and then work back to determine how you’ll achieve that: how much will it cost, how much do you need to borrow, and how much will you need to save?

Rather than just daydreaming about buying a home one day start with a definite goal, such as “I want to buy an apartment in an inner-city suburb by 2020″. Then work back to determine how you’ll achieve that: how much will it cost, how much do you need to borrow, and how much will you need to save?

If the figures seem astronomical, you’ll have to scale down your expectations.

It might be nice to have a trendy inner-city pad, but as a first homebuyer you have to set your sights on something a little more humble to begin with. Most people can’t buy their dream home the first time around.

If this doesn’t sound appealing consider “rentvesting“, which is where you buy an investment property first – in an area you can afford – and your own home later.

The key is to just get a foothold in the market – as long as you can cope with the ongoing commitment – and many are increasingly jumping on the rentvestor bandwagon to do just that. Mortgage Choice figures show almost a third of investors fell into this category last year, up from 20 per cent two years prior.

While we’re thinking outside the box, as a low-income earner you should also consider partnering up with friends or family. You could also borrow from the bank of mum and dad or ask for their help by either by bringing forward your inheritance, having them go as guarantor or staying at home for longer.

No matter what creative avenues you explore, you’ll still need to hone your savings skills to accumulate a deposit and prove to lenders that you’re a safe bet.

Investigate ways to increase your income, such as setting up a home business or doing dog-sitting in your free time to rake in some extra cash.

Do you need to eat baked beans for breakfast, lunch and dinner? Well… maybe just a meal here or there! And you should certainly cut back on smashed avo.

{kind=link}